The third quarter performed exceptionally well and surprised with low volatility and sustained gains in almost all markets. This is unusual, as the third quarter is often characterized by higher volatility and sharp declines. I remember my personal trauma from 1998, when a crisis in Russia severely disrupted my vacation on Lesbos.

In addition to regional changes, the so-called factor rotation is also intensifying, meaning that stocks that represent the quality factor (my favourite factor) are being ignored due to their high valuations.

But this year, everything was different, probably because global central banks are still cutting interest rates or at least considering further rate cuts. This is always a good environment for financial investments.

In contrast, stocks that represent the so-called value factor (low valuations) have become very popular. The same applies to stocks of smaller companies, which are having a very good year, especially outside the United States. I had actually counted the stocks of small companies in America among the “Trump winners,” since Trump is committed to promoting the American industry.

Only Indian stocks and stocks from the healthcare sector are lagging behind the market. The same applies to long-term European and American government bonds. The latter are suffering in particular from the fact that debt ratios in developed countries are now very high. Many bond investors are therefore wondering how this debt can be repaid when governments want to increase their spending on defense and pension payments at the same time!

Nevertheless, small companies in America still seem to be suffering from high interest rates and will probably only see significant price gains once the Fed lowers interest rates even further. This can be assumed, unless there is unexpectedly bad news on inflation, which would make it impossible even for a Trump-friendly Fed to lower interest rates towards 3%.

This skepticism toward long-term government bonds may also be the reason why corporate bonds are in high demand and comparatively expensive American stocks continue to be bought. Investors are simply looking for reliable alternatives, which certainly explains the positive performance of gold and Bitcoin.

International investors are reorienting themselves and reducing their investments in the United States and the U.S. dollar. The beneficiaries are virtually all international stock and bond markets, from Europe to developed Asia and the long-neglected developing countries. In my view, this is a positive development, as many investors tended to ignore obvious opportunities outside the U.S. and developed an almost blind faith in the dominance of the American financial markets. Who would have thought that European bank stocks would outperform Nvidia and Co. this year?

Even though we will only find out over the next few months to what extent Trump’s erratic tariff policy is influencing inflation in America, there are already clear signs of weakness in the American labor market, so that the trend towards lower interest rates can certainly be considered intact.

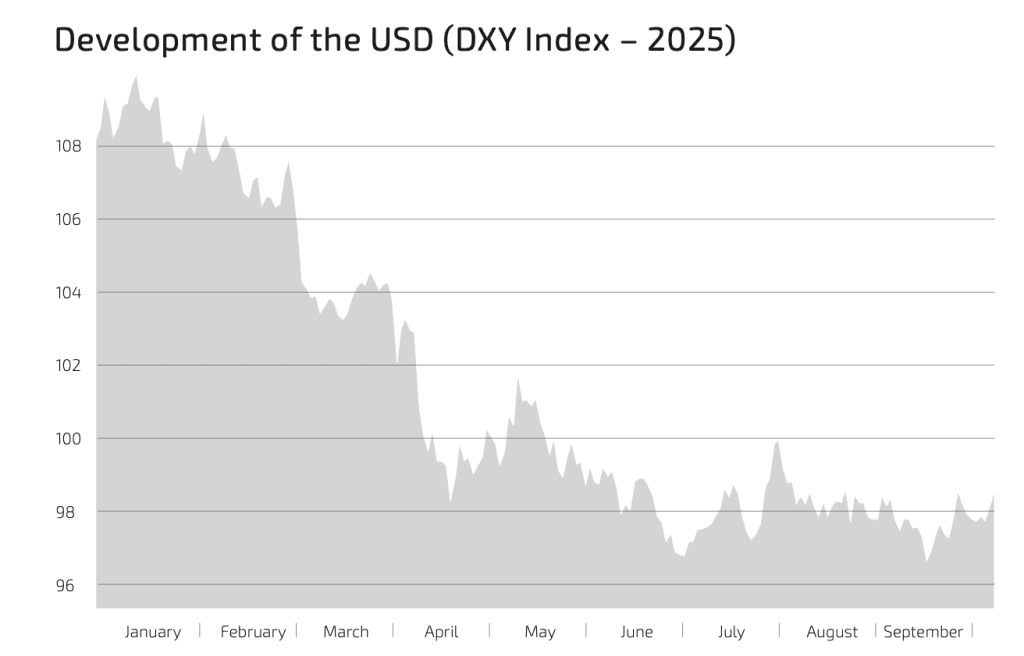

Even though the financial markets appear to be very stable after three quarters, there is one major loser that we cannot ignore: The U.S. dollar has fallen sharply against many global currencies, especially the Euro, and has lost almost 12% since the beginning of the year as measured by the DXY index. Against the Euro, the loss is even closer to 15%.

This significantly reduces the returns of many asset classes for Euro and non-USD investors and dampens the celebratory mood somewhat. Nevertheless, our community members have had a good to very good investment year so far.

Date source: Bloomberg

As far as the most popular equity factors based on the MSCI index family (momentum, size, value, and quality) are concerned, it can be seen that the so-called quality factor, as well as the size factor (company size), underperformed the MSCI World Index, which is calculated on the basis of market capitalization. The so-called value factor (low book value) and the momentum factor (rising prices lead to further price increases) as well as the multi-factor approach (all four factors equally weighted) performed well. The value factor in particular has had a very good year so far and is experiencing something of a renaissance after many years of disappointment.

When comparing index and actively managed strategies, we can state that almost all active bond strategies outperformed their benchmark indices over the course of the year. An investment in active funds was therefore better than an investment in index funds or ETFs.

Among active equity managers, the majority of portfolios also outperformed their benchmark indices. The negative exceptions here are the building blocks O9-A, O10-A (BNY Mellon/Walter Scott) and O14-A (Fundsmith).

We have been monitoring these components for some time and have now decided to replace them with better active components from Fisher Institutional (O20-A), Egerton (O24-A) and others.

Focus on Bonds

After the ECB had already lowered its key interest rates, the U.S. Federal Reserve followed suit in September and implemented a so-called “safety cut.” That was despite the fact that various Fed members want to delay further interest rate cuts until they see how the combination of higher tariffs and a weakening labor market will affect U.S. inflation. This will certainly only become clear at the end of the year or in early 2026.

However, the general climate of interest rate cuts resulted in favorable bond markets at the end of the third quarter, which is why all of our safety components recorded good to very good gains.

Only long-term government bonds showed some volatility and were on the verge of breaking the 5% handle. That said, as of the end of Q3, they’re also showing gains for the year.

Interestingly, bond components that primarily reflect corporate bonds have performed better than government bonds. This clearly shows that many companies now enjoy greater confidence than many countries. This is a new perspective that we may have to get used to.

Safety components with money market securities, variable interest rates, or short maturities, which we use as “flexible piggy banks” (P5 to P7), have all posted price gains because they benefit from stable interest rates and do not carry any significant drawdown risks due to their very low duration.

However, the excellent performance of the Pimco Income (B15-A) component and the actively managed components from Vanguard (B4-A Global Credit and G3-A Emerging Market Bonds) should definitely be mentioned. The management teams at both companies are reliable partners for our community and are managing to navigate the current inflation uncertainty well!

The same applies to the portfolio components Portfolio 1-3. In addition to bonds, the Portfolios 2 and P3 also include a small equity allocation. Experience shows that investors who want to beat inflation and earn attractive equity premiums over the long term should increase the equity allocation of their portfolios in line with their investment horizon. That is why even cautious investors are advised to hold a certain proportion of equities!

Focus on Equities

After many high return components still showed losses at the end of the first half of the year, these were largely offset in the third quarter. Only Indian equities are still loss making as of now.

The global growth and quality strategies that I personally value and prefer, such as the MSCI World Quality Factor ETF (O19-F), Threadneedle Global Focus (O11-A) and Wellington Global Quality Growth (O12-A) are underperforming the broad market in 2025. This is largely a function of their still high valuations, which the market needs to digest. In the long term, all of our quality managers and strategies have outperformed the broadly diversified indices and are entitled to be represented in our building block universe. Nevertheless, we would not currently invest fresh money in these building blocks, as they are still highly valued. However, we would hold these positions with the exception of the BNY Global/Walter Scott (O9-A, O10-A) and Fundsmith (O14-A) building blocks. We have identified alternatives for these managers such as Fisher Insitutional and Egerton, as they no longer enjoy our confidence.

As far as the factor investment building blocks of the MSCI family are concerned, i.e., MSCI World Value, Size, Momentum, and Quality (building blocks O17-F to O19-F, O22-F and R4-I/R5-I), all factors except for Quality factor are matching or beating the broad based index MSCI AC World.

The gains of the value factor are particularly encouraging this year, which leads us to wonder whether this is really a sustained trend or whether it will turn out to be a flash in the pan.

Over a ten-year period, only the MSCI Momentum and MSCI Quality indices were able to outperform the broadly diversified MSCI World Index among the very popular and easily investable factors. This explains our general preference for the quality or Warren Buffet factor, which we track via index ETFs and our active managers.

The momentum factor is also very interesting, but there are currently few opportunities (e.g., O17-F and R60-F) to invest wisely. However, the range of options appears to be growing, and we will keep our community informed accordingly.

The multi-factor indices of the Dimensional family, which we use as easily investable standard portfolios (Portfolio 4 to 6), also had a difficult first half of the year, but have since recovered all their losses and are showing clear gains at the end of the third quarter. It should be noted that the Dimensional equity portfolios are very broadly diversified and represent significantly more stocks than the MSCI World or FTSE All World Index (13,000 versus a maximum of 8,800 stocks). They are therefore less heavily invested in the “Magnificent 7” and, in addition to the “value building blocks,” are recommended as a good complement to our popular quality factor building blocks.

of the year, but have since recovered all their losses and are showing clear gains at the end of the third quarter. It should be noted that the Dimensional equity portfolios are very broadly diversified and represent significantly more stocks than the MSCI World or FTSE All World Index (13,000 versus a maximum of 8,800 stocks). They are therefore less heavily invested in the “Magnificent 7” and, in addition to the “value building blocks,” are recommended as a good complement to our popular quality factor building blocks.

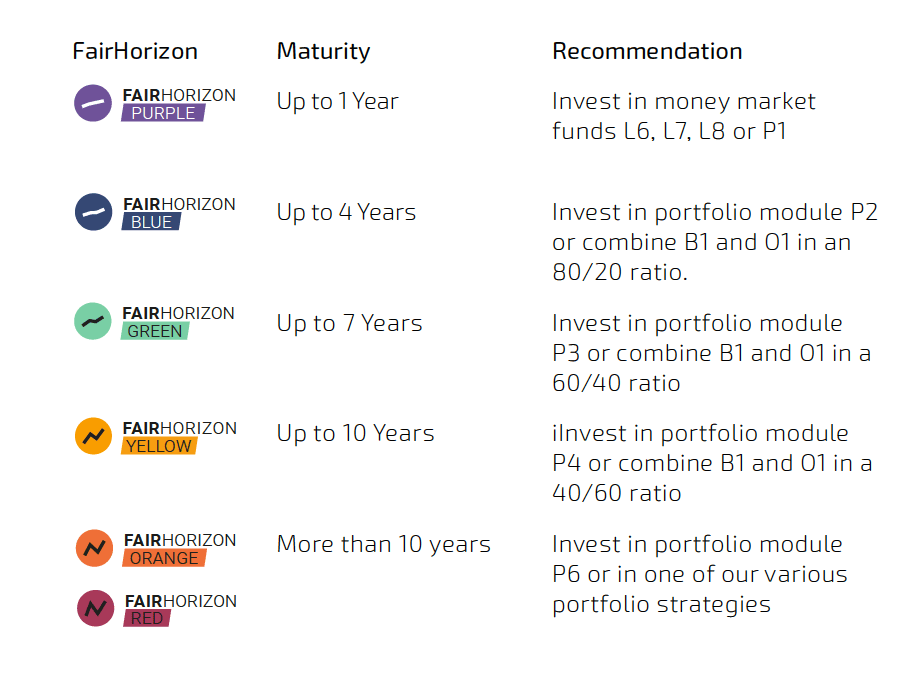

Apart from the performance of the individual components, it is particularly important to combine return and security components to the extent required by the personal situation and expected cash flows of a saver. We have therefore developed the FairHorizon concept (pages 12 & 13) to make it very easy to determine the right combination of ‘safety’ and ‘return’.

Investors therefore need to think carefully about their cash flows and consider when they will need their money. Once this has been clarified, creating the right portfolio is actually child’s play thanks to our color system. As a general rule, the equity component of a portfolio should be increased as the investment period lengthens in order to avoid missing out on returns!

Development of building block combinations

Our combinations of return and security components, which we provide as ideas and model portfolios and which are based on the proven strategies of Jack Bogle (buy the haystack at a low price), Fama/French (optimize the haystack at a low price) and Buffet/Munger/Bessembinder (focus on the flowers in the haystack), have all performed well so far in 2025 and are showing unanimous price gains.

Over the year as a whole, Jack Bogle’s simple index strategy is clearly ahead in terms of equity strategies, while the Buffet strategy is clearly behind. In bond-heavy strategies, active managers are ahead and index strategies are clearly behind.

Each strategy (standard index, factor index, single factor index, or manager) has its day in the sun and works well in the long term in achieving the savings goals of our community. The strategies should therefore not be changed, as it is not possible to determine which strategy might come out on top in the short term.

Other asset classes

Industrial and agriculture commodities, which would normally also be considered a diversifier away from traditional assets, haven’t had a particularly good year.

Gold, on the other hand, has had another spectacular year so far, which makes it clear that the non-U.S. dollar-based world is looking for alternatives. The same applies to Bitcoin, which reached a new high today.

Global real estate markets appear to be stabilizing, and private market investments (private equity, private credit, private infrastructure) have also had a good year thus far.

Outlook for the Coming Months

After the third quarter turned out to be very positive, contrary to expectations, and there were no significant “Trump disruptions” on the financial markets, a certain fear of missing out (FOMO) is spreading in some submarkets. FOMO appears to be particularly pronounced in the global gold market.

FOMO and Panic buying is never good, as it tempts people to switch off their brains and simply do things because others are doing them too. If you do not currently have any gold in your portfolio, please accept that this opportunity has passed you by. Perhaps it will reassure you to know that the long-term performance of a well diversified equity portfolio has matched the returns on gold in recent decades and has even clearly outperformed it in the long term.

The sharp rise in gold prices significantly exceeds the development of global inflation rates of late, and the price charts for gold and gold mining stocks show a technical formation which resembles an antenna, which usually indicates a strong overvaluation.

So please be strong and let the gold train pass you by. If you own gold, just be happy and hold on to it, because there are good reasons to have a certain amount of gold in your portfolio; but not at any price!

Apart from gold, current market valuations remain fair or attractive, with the exception of expensive American technology favorites. In my opinion, the revaluation of Asian and European stocks is still in its early stages, which is why I have no concerns if community members want to get involved here.

The same applies to Latin American stocks and stocks of small and medium-sized American companies. Anyone buying here should feel confident, based on current valuations, that the expected risk premiums of 6-8% p.a. can be achieved.

Those who still want to invest in technology stocks should take a look at our CT Global Technology portfolio (R45-A). Its manager Ben Wick has been managing technology stocks since the 1990s and has even managed to beat the popular Nasdaq 100 with his fund. This year, he has clearly outperformed the Nasdaq 100. The portfolio is significantly better diversified than the Nasdaq 100, and Mr. Wick’s active management has also performed very well in times of crisis.

Pages 9-11 of this publication show our high-rise charts and the valuation traffic lights next to the individual building blocks and strategies. Please use this information to review your portfolios.However, this does not necessarily mean that your chosen strategy needs to be changed. But if you are sitting on high gains and are heavily invested in investments such as the Nasdaq 100, the S&P 500, the MSCI World, and the MSCI World Quality Index, you should consider rebalancing into more favorably valued equity ideas.

All other components are either moderately or favorably valued, meaning they can continue to be purchased without any concerns.

Even though the highly valued market segments are susceptible to setbacks, we would advise against changing your strategy or exiting the market on an emotional basis only to re-enter later.

The performance of our reference portfolios on page 14 speaks for itself. Those who approach the financial markets with a certain degree of optimism will clearly be rewarded!

Even though we are still assessing the long-term impact of Trump’s tariff policy on global inflation rates, the Fed’s significant scope for lowering interest rates should provide solid support for the market. Added to this is the fact that the fourth quarter of the year is usually characterized by stability and gains. From this perspective, we can look forward to the end of the year with confidence.

It is important to structure a long-term portfolio around an investor’s personal situation, income and investment horizon.

With the applied knowledge and experience of these giants of the capital market in combination with our FairHorizons, there’s not much that can go wrong.

All you must do is think specifically about your cash flows and investment time horizon and create a portfolio on this basis. Our colour system shows you the way!

In times of rising interest rates, make sure that you do not take on too much credit. Loans with interest rates of well over 7% p.a. should always be repaid first before savings concepts are tackled. Otherwise, you will end up in the hamster wheel of negative compound interest!

Please contact us if you have any questions or concerns. We are always here for you!

With best wishes for a great final quarter of 2025!