Background – The ‘TACO Trade’ rules financial markets!

After global markets were thrown into turmoil because of the so-called Liberation Day on 2 April, an astonishing calm has set in:

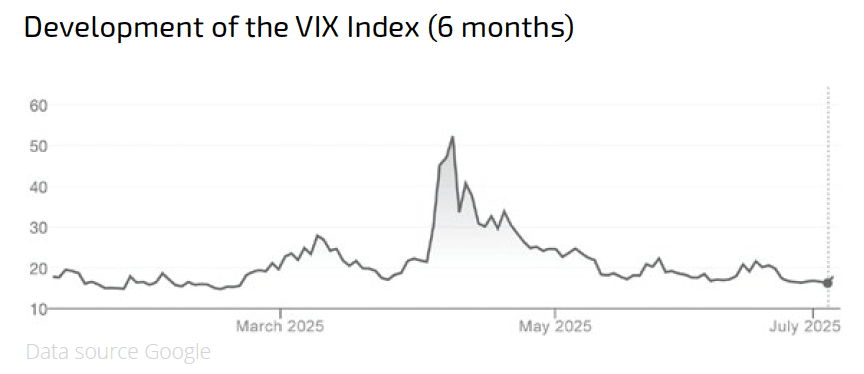

Market volatility, which is measured by the ‘VIX Index’ (volatility of the S&P 500 Index), had reached extreme values of over 50 on April 7th, and is currently back at just under 17. That’s well within the normal range of 10 to 25, which we have witnessed in recent years.

- Important global stock indices such as the MSCI World, the S&P 500 and the Nasdaq 100 Index have recovered or even exceeded their highs of 19 February.

- Bond markets have stabilised; even at the so-called long end, i.e. bonds with very long maturities, have not seen further increases in yields. This is a big surprise, as the expected passing of the so-called ‘Big Beautiful Bill’ is widely perceived as inflationary.

How can all this be explained if no reliable agreements have been reached on US tariffs, whilst a long-feared military conflict between Iran and America took place!?

Presumably it is because Trump suspended the higher tariffs because of the collapse in share prices at the beginning of April, thereby making it clear that he ultimately has the well-being of financial markets very much at heart.

This wasn’t so clear in the days following 2 April. For a few days, it looked as if Trump had turned from market-focused capitalist to political demagogue. This caused a huge scare in the international financial community and probably triggered the sharp fall in global share prices. In the meantime, however, the American president has shown that he is ‘back to his old self,’ i.e. keen to please financial markets, which is why confidence and calm have returned.

Robert Armstrong, a columnist for the Financial Times, has used the April turn-around to coin the phrase ‘TACO’ or ‘Trump Always Chickens Out.’ It means that Trump changes his mind very quickly when his decisions have negative effects on stocks and bonds. He likes to be associated with buoyant markets, which became very clear in his first presidency.

That’s why many market participants were shocked to see that Trump seemingly ignored the obvious repercussions on markets when he announced his excessive tariffs. Luckily, he ‘chickened out’, so we could all enjoy the TACO Trade!

Even if markets appear eerily calm by mid-year, there is one big loser that we cannot ignore:

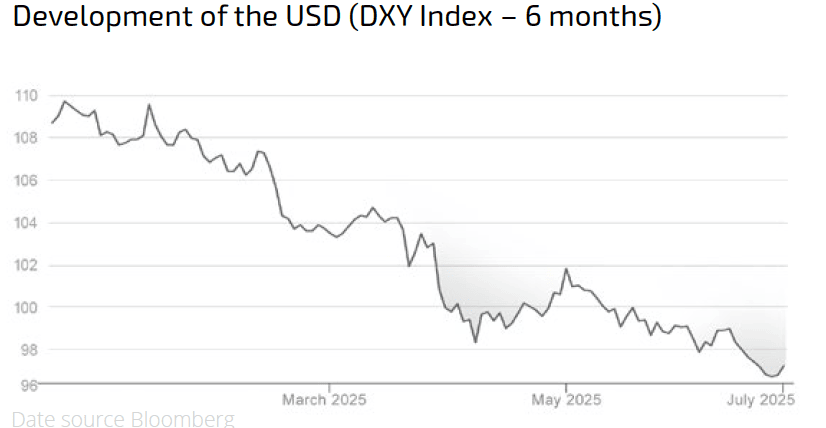

The US dollar has fallen sharply against many global currencies and is down almost 15% since the beginning of the year as measured by the DXY Index. This clearly shows that Trump‘s policies are ultimately having a negative impact on America‘s position within the international community, which is why global investors are looking for alternatives to American assets.

After all, what good is a new high in the S&P 500 to international investors if at the same time they experience currency losses of more than 10%!? Donald Trump and his team have destroyed a lot of trust, and the U.S. currency is reflecting that. Anyone using the DXY index as a guide will realise that there could still be considerable downside potential from here, even if there will be counter movements at times.

In addition to the valuations of asset classes, the future development of the Dollar exchange rate will determine the direction of our portfolios. That is something we could ignore in times of Dollar strength but need to bring back to our portfolio construction toolkit.

Next to the U.S. Dollar and portfolios that are heavily weighted in U.S. dollar, we must also note that shares in the healthcare sector as well as the shares of small and medium-sized American companies, as measured by the S&P 600, S&P 400 and the Russell 2000 Index, are among the losers at mid-year. This is perhaps not a surprise if we look at the pharmaceutical sector, as the Trump administration wants to contain healthcare costs, which may have a detrimental impact on the earnings of healthcare businesses. We have witnessed something similar in the 1990s when President Clinton was trying to contain healthcare costs.

However, there is no such explanation for the losses of shares of small and medium-sized companies.

The multi-factor indices of the Dimensional family, which we use as easily investable standard portfolios (Portfolio 4 to Portfolio 6), were able to hold their ground and showed some outperformance against the standard indices of the MSCI and FTSE Russell families. It should be noted that the Dimensional equity portfolios are very broadly diversified and cover considerably more stocks than the MSCI World or the FTSE All World Index (e.g. 13,000 versus a maximum of 8,800 stocks). They are therefore less heavily invested in the ‘Magnificent 7’ and are complementing our popular quality factor modules very well.

Other asset classes

Away from traditional asset classes such as equities and bonds, commodities did not perform well in the first half of the year, especially if calculated in European or Asian currencies. Gold, on the other hand, had another very good period, which clearly shows that the non-Dollar based world is looking for alternatives. The same applies to Bitcoin, which has since reached a new high. In contrast to Bitcoin, however, the so-called alternative coins (alt coins) have mostly experienced losses. This reminds me of the fact that it seldom pays to switch gold into silver or platinum, just because they’re lagging in performance. Only gold and potentially Bitcoin seem to be really seen as the ‘Anti Dollar.’

The global real estate markets appear to be stabilising, and private market investments (private equity, private credit, private infrastructure) also had a good first half of 2025. Listed private equity companies didn’t do as well but were also considered overbought.

In recent years it was better to buy shares of private asset managers than buying their investment funds. Given the difference in valuations, it may now be better to buy high quality private equity funds rather than the shares of private equity managers.

Active versus passive investing

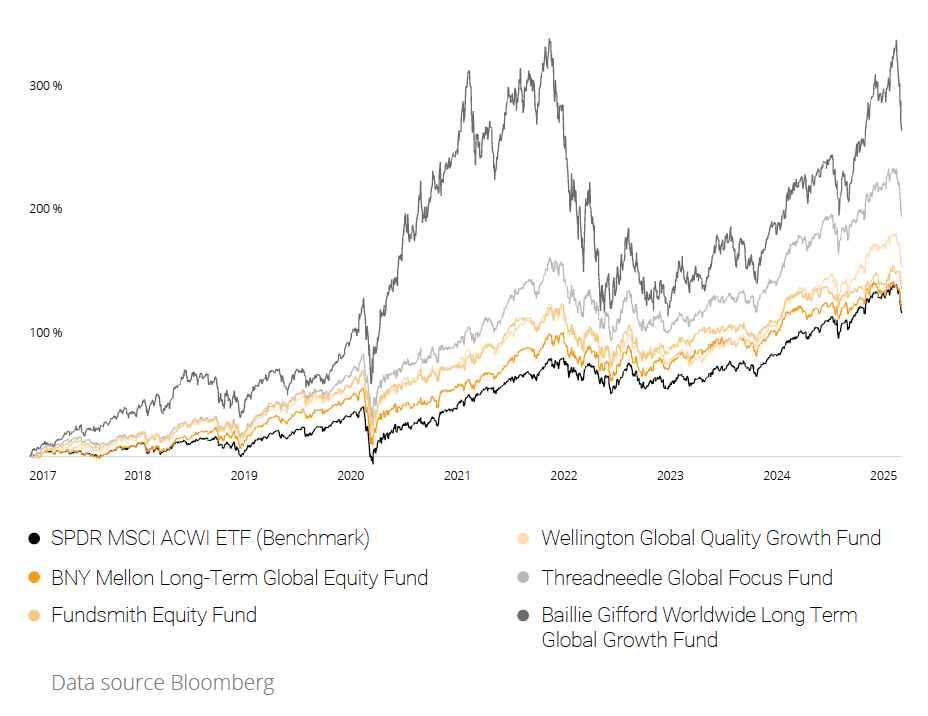

As far as the comparison between index investing and actively managed strategies is concerned, almost all active bond strategies outperformed their benchmark indices over the course of the year. An investment in active funds was therefore better than an investment in index funds or ETFs. In the case of active equity managers, most portfolios also matched or outperformed their benchmark indices. The negative exceptions here are the building blocks O9-A/O10-A (BNY Mellon/Walter Scott), O13-A (Amundi Polen), O14-A (Fundsmith) and R6-A (CT Global Smaller Companies).

We have been monitoring these modules for some time and have now decided to replace them with better active modules. Over the next few weeks, we will be contacting all clients who have these building blocks in their portfolios to draw their attention to suitable alternatives.

Development of portfolio building blocks and building block combinations

Our combinations of return and security building blocks, which we have available as ideas and sample portfolios and in which we rely on the proven strategies of Jack Bogle (buy the haystack at a low price), Fama/French (optimise the haystack at a low price) and Buffett/Munger/Bessembinder (focus on the flowers in the haystack and don’t overpay), have all done well so far in 2025. The multi-factor strategy, which follows Fama/French, seems to have a slight edge.

The only but significant caveat is the fact that non-U.S. Dollar investors will look at these numbers rather differently since they will have to add currency losses of sometimes more than 10%. This can be very painful. The general rule for portfolio construction is that global equity exposure should normally not be hedged back into an investor’s reference currency as globally diversified portfolios are balancing currency gains and losses. We would however hedge the fixed income allocation back into an investor’s reference currency as fixed income is typically meant to stabilise a portfolio and to enable consumption in the reference currency.

We are very pleased that the portfolios of our client community are developing well and deliver on expectations.

Please don’t hesitate to reach out to us and become part of our DFO Community!

Outlook for the Coming Months

A good first half-year lies behind us and has once again shown that it makes sense to stick stoically to a well-designed portfolio strategy. Even if Donald Trump sends us news every day, we should not let this unsettle our portfolios. High portfolio turnover normally leads to underperformance.

Now that global equity markets have almost completely recovered from the April 7th correction, investors are once again presented with an opportunity to rebalance portfolios that are heavily invested in popular American equities such as the Magnificent 7. The same applies to portfolios that are heavily weighted in U.S. dollar investments and could cause further losses for non-Dollar investors. This is particularly important for our community members who are based in Euro, Pound Sterling, Singapore Dollar or other Asian currencies.

The pages 8 to 10 of this publication show our high-rise charts, and the valuation traffic lights next to the individual investment components. Please use this information to review your portfolios and rebalance away from expensive investments towards better valued markets, sectors or factors.

This is by no means intended to imply that your chosen strategy needs to be changed. However, if you are sitting on significant gains and are heavily exposed to investments such as the Nasdaq 100, the S&P 500, the MSCI World and the MSCI World Quality Index, you should consider rebalancing your equity portfolio. All other building blocks are either moderately or favourably valued, so that they can continue to be bought without any doubt.

Even though the summer months are often accompanied by higher market volatility and whilst expensive market segments are susceptible to setbacks, we would advise against changing your strategy or exiting the market altogether, just because ‘it feels right.’ The long-term performance of our investment universe speaks for itself. If you approach the financial markets with a certain optimism, you will be rewarded!

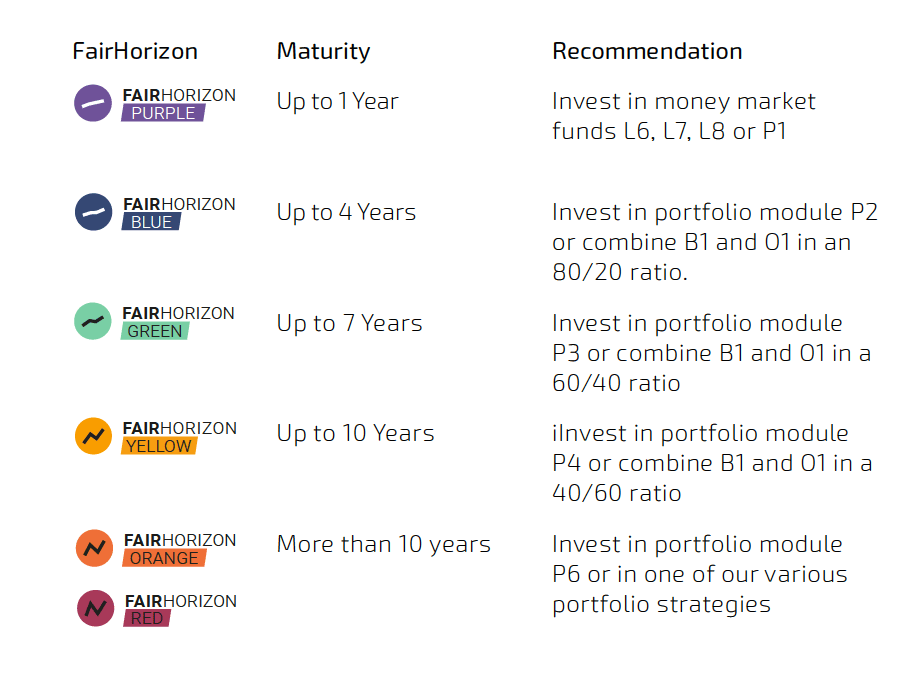

The expiry of the interim deadline for US tariffs on 8 July could result in short-term volatility spikes. This may be counteracted by the fact that inflation seems contained, which allows central banks to cut their reference rates even further. So, despite the current political noise, investors are faced with a relatively normal financial market and should therefore not hesitate to build solid portfolios based on our FairHorizon concept (page 11).

It is important to organise a long-term portfolio in such a way that it takes account of the investor‘s personal situation, income and a realistic investment horizon. With the applied knowledge and experience of these giants of the capital market in combination with our FairHorizons, there‘s not much that can go wrong.

All you must do is think specifically about your cash flows and investment time horizon and create a portfolio on this basis. Our colour system shows you the way!

In times of rising interest rates, make sure that you do not take on too much credit. Loans with interest rates of well over 7% p.a. should always be repaid first before savings concepts are tackled. Otherwise, you will end up in the hamster wheel of negative compound interest!

Please contact us if you have any questions or concerns. We are always here for you!

With best wishes for a great summer!