Waiting for a correction that never comes?

After an unexpectedly strong September, global financial markets also enjoyed a good October. Technology stocks in the United States and Asia in particular recorded sharp gains in some cases, which boosted both the sector and the many indices in which technology stocks are heavily weighted. These include the Nasdaq 100, the S&P 500, the MSCI World, but also the Nikkei 225 and the MSCI Korea and Taiwan.

In the less technology-heavy markets, the month was somewhat quieter but also positive. The two German indices, the DAX and MDAX, have been moving sideways for months now, digesting the strong gains of the first months of the year.

India had a good October but is still down since the beginning of the year. The same applies to real estate, private equity, and healthcare stocks.

The global bond market also had a good month, recording gains across the entire maturity spectrum. The same could be seen for corporate and emerging-market bonds. Even long-dated government bonds, which had been less in demand in previous months, recorded gains, although they are still significantly down since the beginning of the year.

Commodities also performed well, with gold rallying to a provisional high of just under USD 4,400 per troy ounce before entering a consolidation phase.

The US dollar recorded gains against the euro and other G10 currencies, except for the Japanese yen. The relevant DXY Index has now stabilised at around 97 points, suggesting that the US dollar’s weakness this year may be coming to an end.

Europe’s outperformance of US stocks weakens

Europe’s outperformance of US stocks since the beginning of the year clearly weakened in October, even though European equities still appear very attractive. The same applies to Asian and Latin American stocks, which are benefiting from an ongoing rotation out of America and are still attractively valued.

Due to the massive recovery of global tech stocks in October, we are now in some cases above the valuation levels seen at the end of March, when we criticised the high valuations of the Magnificent 7.

Risk premiums have again melted away from 5.5% p.a. in April to less than 4% p.a., which again prompts us to exercise caution. At these levels, we would not buy the S&P 500 Index, the Nasdaq 100 Index, or similarly oriented technology funds or ETFs. The same applies to the traditional MSCI World Index.

Currently, we can only recommend the MSCI ACWI IMI, which has a significantly lower proportion of large American companies and invests significantly in developing countries and small companies.

The same applies to the STOXX World Multifactor Index, which is also suitable for investors who want to achieve a global asset allocation by buying just a few building blocks.

Our clients who are already heavily invested in global tech have started rebalancing into less expensive markets such as global small caps, healthcare, and emerging markets, which are now also available via EM value-factor ETFs.

Outside the Magnificent 7 and certain meme stocks, which have once again overheated, valuations generally look more moderate to favourable.

Especially equity strategies that focus on low valuations and income (value or dividend strategies) are attractive. The same applies to equities from developing countries, Europe, and Asia (see high-rise charts on pages 5 and 6).

Bonds, India, and client guidance

In India, the current correction seems to be slowly coming to an end, which is why we would consider re-engaging here.

Bonds still appear very attractive, especially when compared to current or expected inflation rates. High-quality bonds should also benefit if the US economy were to move into a recession.

In this context, I would also like to point out that our standard building blocks from Dimensional (Portfolios 1 to 6) are fundamentally very broadly positioned and were never overly invested in America.

Clients who are already invested here can therefore rest easy, while others who may have found these building blocks too “boring” up to now should take a second look at them.

In my opinion, the best orientation for the composition of a new portfolio is the current valuation of an investment. This is because the valuation of an investment is a good indicator of the expected ten-year return.

We have therefore supplemented our high-rise charts with the valuation traffic light. This traffic light has worked very well so far because high valuations (red) inevitably entail a higher risk of losses and lower expected returns than normal (yellow) or favourable (green) valuations. Therefore, please use our valuation traffic light for future investment decisions!

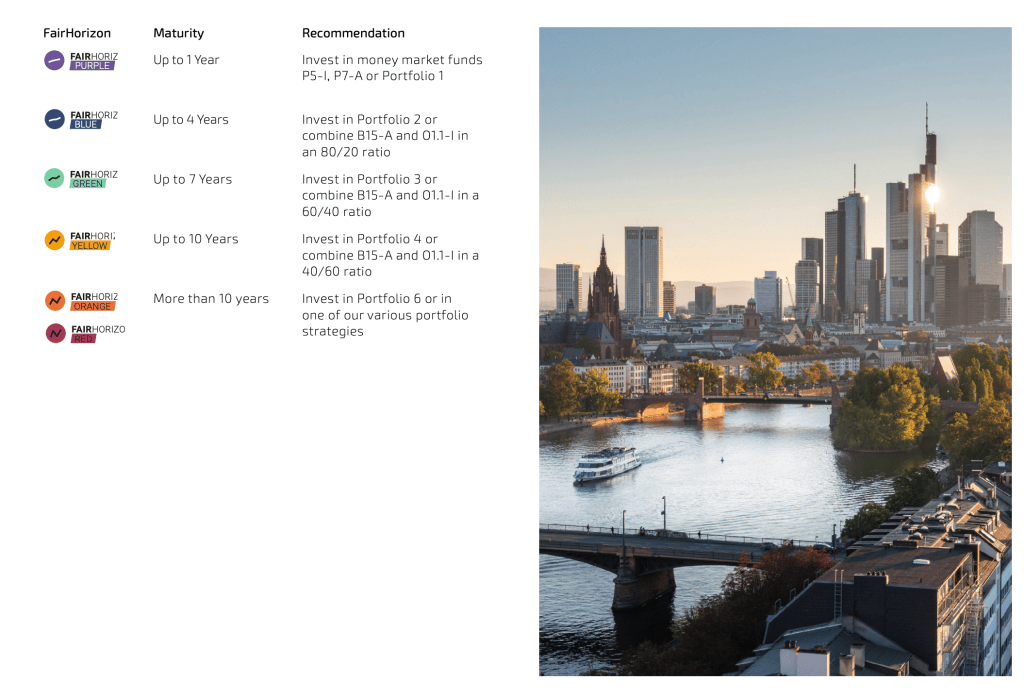

For “fresh money,” we recommend our proven concept of FairHorizons, which we have developed based on established asset-allocation principles. It offers a simple way of creating portfolios that can beat inflation and earn attractive risk premiums.

Please also look at our standard investment portfolio ideas on pages 29 to 31, which follow the principles of investment legends like Jack Bogle, Eugene Fama/Kenneth French, and Warren Buffett. Whilst all of them represent different investment philosophies, they are all very effective and successful in the long term.

If you are worried whether your portfolio is well equipped for the significant changes in today’s world, just get in touch with us. We will be more than happy to check for you.

Otherwise, I would be delighted if you could tell your friends and family about Das Family Office so that they can also become part of our community.

With best wishes for a pleasant end of the year!

Yours,

Mario Becker

Das Family Office