The beginning of a long-overdue correction in the AI sector…

Global financial markets in November were more reminiscent of August or September, months traditionally associated with increased volatility. Thus, 2025 is proving to be a year that is in many ways different from what usual seasonality would suggest.

However, if you look at the monthly results of our advisory universe, you will see that November was a decent month which mostly produced gains for investors. Only long-term government bonds and heavily technology-oriented investments saw losses.

AI sector: clouds on the horizon

This was because dark clouds are gathering on the horizon for AI investors. The rally of Nvidia, Oracle and their ilk, i.e. the suppliers of the AI world, came to an abrupt halt in November.

With the launch of Gemini 3.0, Alphabet/Google seems to be showing, next to Chinese providers such as DeepSeek, that it is possible to develop very good models that are superior to the current Chat GPT version, even without expensive GPUs from Nvidia.

This calls into question the assumption that modern AI data centres require almost unlimited computing power.

Since Nvidia is heavily represented in many technology portfolios and broad-based indices, our building blocks, which are primarily focused on this trend, suffered losses.

The same applies to familiar technology indices such as the Nasdaq 100 as well as the country indices of Taiwan and Korea, both of which are dominated by chip manufacturers such as TSMC and Samsung & Hynix, respectively.

Sector rotation: healthcare & Swiss equities shine

In contrast to the weak performance of AI stocks, there was a rally in the healthcare sector, which benefited our two building blocks for biotech (Polar) and healthcare (Alliance Bernstein).

This once again demonstrated that sector investments can lag the market for a long time, but then rise very sharply for no apparent reason. They must therefore be understood as long-term investments, and their managers or indices should not be doubted despite short-term disappointments.

Swiss equities also had a good November, partly because the Swiss index is relatively cheap and dominated by value and healthcare stocks. On the other hand, Switzerland was able to agree on a new tariff solution with the United States, which removes uncertainty from its market.

Small caps, value & dividends: beneficiaries of rate hopes

Shares in smaller companies also had a good month, especially once it became clear that the FED may cut interest rates further in December. Small Cap stocks are highly sensitive to interest rate movements and seem to benefit again, now that the rate cutting trend has been re-established.

I generally recommend small and medium sized company stocks as an addition to a portfolio, even though they often perform differently from the broader market and therefore harbour potential for short-term disappointment. In the long term, however, they are good for a few extra points of return and have their place in strategic asset allocation decisions.

Equity components that pursue value or dividend strategies also had a good November. This shows once again that value complements growth, quality and momentum strategies very well.

Bonds, commodities and gold

The global bond market also had a positive month, with gains across the entire maturity spectrum, except for long-term government bonds. Corporate and emerging market bonds were also up in November!

Commodities and gold remained stable. The question now is whether October’s gold correction is already over or whether there will be further testing of the USD 4,000 per troy ounce level.

As already announced in our podcast, we have added two ETFs on gold mining stocks to our programme (Tickers GDX:LN and GDXJ:LN). Even though gold mining stocks have tended to disappoint in the long term, mining companies are currently able to generate substantial cash flow and appear to be attractively valued. This situation is only expected to change if the price of gold falls significantly below USD 3,000 per troy ounce, which is currently considered unlikely.

However, we would limit exposure to gold and gold mining stocks to around 10–15% of a portfolio, as the gold market has historically failed to match the returns of quality stocks. Nevertheless, gold investments have historically proven to be a good complement to equities and real estate.

US dollar weakness and regional equity positioning

The US dollar had stabilised at around 100 based on the DXY index but has been trending slightly weaker again since US labour market data points to a rise in unemployment. This opens the door to further interest rate cuts by the Fed, which is likely to weigh on the US dollar.

We should therefore expect further dollar weakness and adjust our portfolios accordingly. In concrete terms, this means reducing American equities to around 50% of a portfolio.

European equities and equities from developing countries and Asia remain attractively valued, which is why portfolio adjustments should be undertaken at current price levels.

We’ve recently been buying Asian and Latin American equities as well as European momentum strategies and bank stocks as diversifiers.

Technology valuations and the CT Global Technology Fund

Despite the small correction in November, many technology equities are still in the red on our valuation traffic light and therefore at a level that we consider unattractive. Equities such as Nvidia and Microsoft also look technically weak, which harbours further potential for disappointment. The same applies to the Nasdaq 100 Index.

At current valuation levels, technology investors may rather consider the CT Global Technology Fund, which, with a free cash flow yield of 3.5% p.a., is valued 40% lower than the Nasdaq 100. The fund has clearly outperformed the Nasdaq 100 this year and has also beaten the index over the past two decades.

We are very fond of the manager, Paul Wick, who’s been managing tech stocks since the early 90s. Our positive opinion has been reinforced after meeting him in person a few weeks ago.

Where valuations still look attractive

Apart from the expensive AI and Magnificent 7 market segments, valuations generally look moderate to favourable.

Bonds still appear attractive, especially when compared to current or expected inflation rates.

Equity strategies that focus on low valuations and income (value or dividend strategies) are also relatively cheap. The same applies to equities from developing countries, Europe and Asia. (See high-rise charts on pages 5 and 6).

In India, the correction seems to have come to an end, not least due to better valuations. We would consider re-engaging here and have added Jupiter India as an institutional share class to our advisory universe.

Indian equities have proven to be a sensible strategic allocation for long-term investors. They differ greatly from Chinese equities, which are more likely to be seen as trading instruments.

Dimensional building blocks: broad, boring – and effective

In this context, I would also like to point out that our standard building blocks from Dimensional (portfolios 1 to 6) are generally very broadly diversified and were never overly invested in America. In November, they all performed positively again, thanks to their very broad diversification.

Community members who have already invested here can therefore rest easy, while community members who may have found these building blocks too “boring” up to now should take a second look at them!

Valuation as a guidepost for portfolio construction

In my opinion, the best orientation for the composition of a new portfolio is the current valuation of an investment. This is because the valuation of an investment is a good indicator of the expected ten-year return.

We have therefore supplemented our high-rise charts with the valuation traffic light. This traffic light has worked very well so far because high valuations (red) inevitably entail a higher risk of losses and lower expected returns than normal (yellow) or favourable (green) valuations.

Therefore, please use our valuation traffic light for future investment decisions!

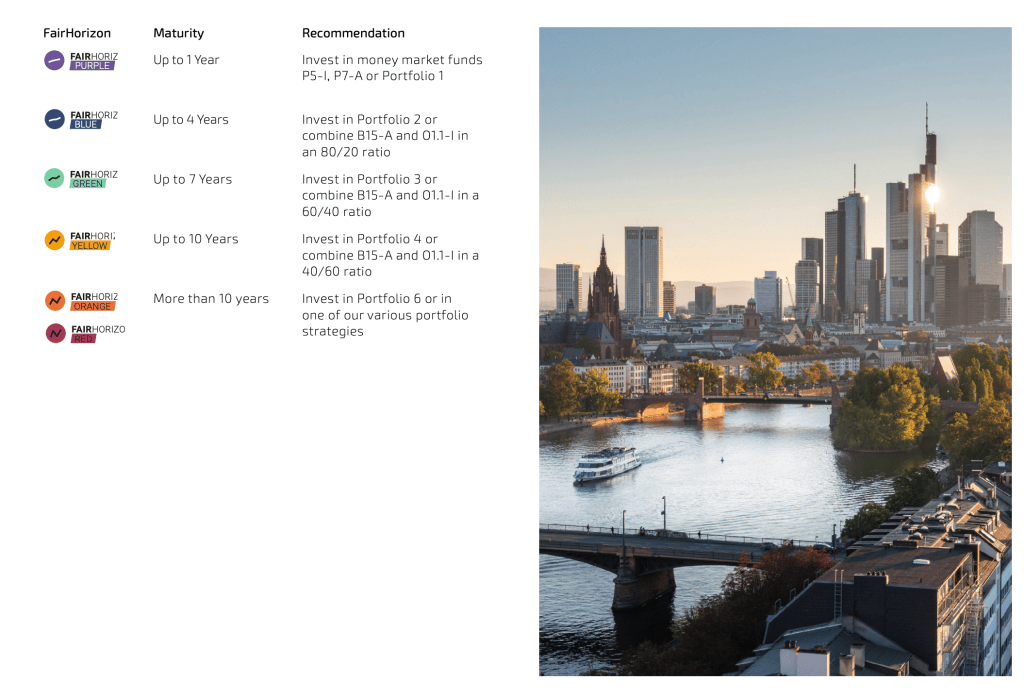

‘Fresh money’ and the FairHorizons concept

For ‘fresh money’, we recommend our proven concept of FairHorizons, which we have developed based on established asset allocation principles. It offers a simple way of creating portfolios that can beat inflation and earn attractive risk premiums.

We would suggest the following strategy for the coming quarters as part of the FairHorizon concept:

Please also look at our standard investment portfolio ideas on pages 29 to 31, which follow the principles of investment legends like Jack Bogle, Eugene Fama/Kenneth French and Warren Buffet/Charly Munger. Whilst all of them represent different investment philosophies, they’re all very effective and successful in the long term.

Final thoughts

If you are worried whether your portfolio is well equipped for the significant changes in today’s world, just get in touch with us. We’ll be more than happy to check for you.

Otherwise, I would be delighted if you could tell your friends and family about Das Family Office so that they can also become part of our community.

With best wishes for a quiet ending of the year and joyful celebrations!

Yours,