Review – January at a glance

The positive sentiment on global stock markets continues in January!

Though only four weeks have passed, we have already experienced many unexpected events. Almost every day, news from the White House forces us to consider whether these are important announcements that need to be taken into account in our portfolios or whether they are simply noise.

Fortunately, so far we can say that we should calmly focus on the economic fundamentals, as statements that lead to short-term market turmoil are relatively quickly refuted. So, it’s business as usual in ‘Tacoland’!

Impact of Kevin Warsh’s Appointment

The most important news recently was the appointment of Kevin Warsh, who will replace Jerome Powell as chairman of the Fed. This appointment had been eagerly awaited and resulted in a surprising drop in precious metal prices. Apparently, many market participants had assumed that Trump would appoint an absolute yes-man who would continue to undermine the value of the U.S. dollar through poor central bank policy. However, Kevin Warsh has traditionally been associated with conservative central bank policy and appears to have close ties to Wall Street heavyweights such as Stanley Druckenmiller. Druckenmiller is a recognised figure in financial circles and will certainly be able to exert a positive influence behind the scenes.

In my opinion, this development is very good, as a U.S. dollar spiralling downward would severely damage financial markets. However, the appointment caught many investors off guard, who apparently believed in the sole salvation of gold and silver.

As is so often the case, stock markets do not just rise or fall in one direction!

Global Stock Market Performance

Apart from the rampant speculation in precious metals, many trends from the fourth quarter remained intact or accelerated in January. The German benchmark index, the DAX, like other European stock indices, reached new highs.

Except for India, Asian markets were also very strong. The South Korean Kospi index surpassed the 5,000-point mark for the first time, which the new president had announced as a medium-term goal. In addition to a business-friendly government, speculation on semiconductor manufacturers such as Samsung Electronics and SK Hynix is driving this market. The same applies to Taiwan, whose stock market is significantly influenced by Taiwan Semiconductor. As these stocks are all heavily weighted in emerging market indices, those indices also had a very good January. Latin American stock markets benefited from strong demand for mining companies and banks. Shares in small companies also had a very good January, which is making me increasingly happy, as I had touted the benefits of adding small caps to a strategic asset allocation.

The Shift from ‘Magnificent 7’

As we could already witness in Q4 2025, the ‘Magnificent 7’ are struggling or have gone into reverse. This development is positive, as interest in other market segments is increasing and we are seeing less concentration on just a few companies. Anyone following Microsoft’s share price will notice that the party is probably over for now.

In contrast, the party in markets outside America is still in full swing. Only India and growth stocks, which are heavily represented in the Russell 1000 Growth Index, have had a weak start to the year.

Bond Markets and Real Estate

Global bond markets had a quiet start to the year and were flat to slightly positive for money market and short- to medium-term durations. U.S. dollar investment-grade bonds with longer durations recorded small losses, while investment-grade bond returns in euros were positive across the board. Tier 1 capital and high-yield bonds had a great January in both currencies.

REITs appear to have slowly bottomed out and are off to a good start this year. Valuations are attractive, which opens further upside potential.

Private Equity and Commodity Volatility

Shares in listed private equity companies had a subdued start to the year, despite their weak performance in 2025. There are growing concerns that these companies could indirectly suffer from weak credit markets for software companies, which could come under severe competitive pressure from AI systems. We need to see whether this is scaremongering or whether these risks are real. Unfortunately, this will take a while, and uncertainty leads to weak stock prices. Private equity funds, on the other hand, reported a decent month based on the performance of so-called ‘evergreen structures’.

As in the final quarter of 2025, commodity markets had a strong January, which led to panic buying, especially in precious metals. This buying panic has since been corrected, and it remains to be seen to what extent the market will calm down or whether this was a ‘flash crash’ and we will quickly see new highs for gold and silver.

Buying just because everyone else is buying is generally not a good recipe for long-term investment success, so please be careful not to get sucked into FOMO-driven action. That said, shares of gold and copper mining companies still appear attractively valued and could be added to well-diversified portfolios.

Bitcoin has now fallen below USD 80,000, which was considered an important technical support level. Further support levels lie between USD 60,000 and USD 70,000, but the chart does not look very inviting. So please exercise caution and speculate in mining or semiconductor stocks instead if you feel the urge to trade.

Currency Markets: USD and Yen

As far as currencies are concerned, the U.S. dollar seems to have entered a period of stabilisation after the sell-off at the end of January. The reason for this is probably the appointment of Kevin Warsh as the new Fed chairman.

We are monitoring the Japanese yen for potential gains, now that the interest rate differential with other global currencies has narrowed significantly. As a result, we have exchanged yen loans into Singapore dollars for some clients. The same applies to clients who have loans in Australian dollars. We have encouraged them to switch into HKD or SGD.

Three Investment Philosophies

We generally promote three long-term investment philosophies that have proven robust over time. All three approaches delivered solid results in 2025 and also started 2026 well, although short-term performance differences can always occur.

1) Traditional index investing (Jack Bogle)

Traditional indexing means broadly investing in the market at very low cost. However, many global equity indices are currently heavily dominated by U.S. stocks. While this was beneficial in recent years, it led to relative underperformance at the start of 2026. Indices with less exposure to U.S. equities, such as Europe, Asia, and Emerging Markets, performed significantly better in January.

On the bond side, traditional indices delivered a stable start to the year, with generally small positive returns across most segments.

2) Factor or scientific investing (Eugene Fama / Kenneth French)

Factor investing targets specific characteristics such as value, size, or quality. January 2026 was a strong month for several of these factors. Value stocks again generated noticeable excess returns, continuing their positive trend from 2025. Smaller companies also had a good start to the year globally. After a weak 2025, the quality factor showed clear improvement in January.

In bonds, systematic approaches also had a good start to the year and once again slightly outperformed traditional bond indices.

3) Focused investing in a small number of securities (Warren Buffett / Charlie Munger / Henrik Bessembinder)

This approach relies on carefully selected active managers who concentrate on a limited number of high-conviction investments.

January was another strong month for our preferred active bond managers, who clearly outperformed their benchmarks. Most of our active equity managers also had a good start to the year.

A particularly notable example is Paul Wick from Threadneedle, whose strategy gained around 8% in January, significantly outperforming the Nasdaq 100, which posted a slight loss. This illustrates how active managers can benefit from the current rotation within the technology sector and beyond.

In the very short term, we continue to prefer money market ETFs and index funds. For bonds with normal duration and special situations, we rely on selected active managers at institutional pricing. In equities, we combine factor-based strategies with active management, especially in specific themes such as technology, healthcare, and emerging markets, while traditional broad markets are often covered via index strategies.

Outlook – It’s worth taking a look at valuations

Navigating Market Trends and FOMO

After just under four weeks, we have an initial idea of what the year might bring. The major trend towards diversification away from Large American equities and the U.S. dollar has solidified and is very likely to continue. However, there are already signs that call for caution. Blindly buying commodity stocks, precious metals, or even the very popular semiconductor stocks in Korea and Taiwan could backfire if investors do not also consider their valuations.

So please only buy if you have a well-thought-out idea and valuations are appropriate. Don’t let FOMO tarnish your decisions!

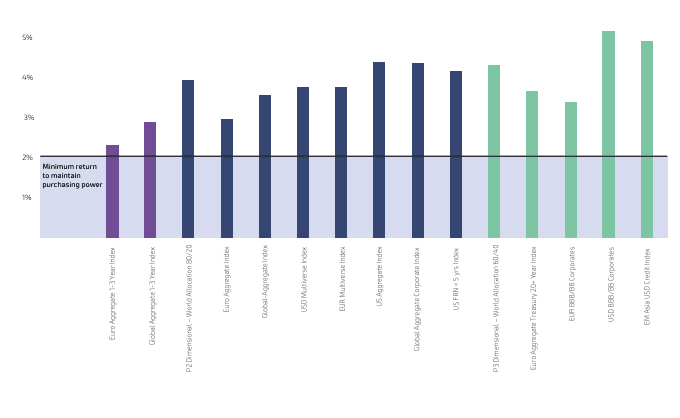

Yields, Inflation, and Purchasing Power

If we look at the current valuations of our high-return and safety components in our high-rise chart (pages 4–7), we are pleased to see that the current yields of the safety components are all above the expected medium-term inflation rate, regardless of the investment horizon (FairHorizons purple to green). Even money market investments are close to current inflation rates and therefore offer purchasing power preservation. This was not the case in the years prior to the adjustment of global interest rates in 2022.

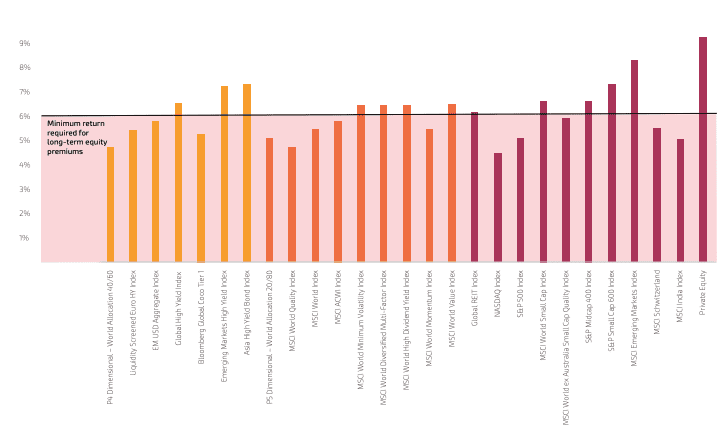

Regarding the return components that we select for longer-term investment horizons (FairHorizons yellow to red), we always communicate a minimum target return of 6% p.a. or a projected long-term return of between 6% and 8% p.a.

Equity Risk Premiums and Regional Opportunities

Due to the positive performance in 2025, the current target returns (or risk premiums) of many return components are now below the 6% mark, which is why we would not be particularly enthusiastic about buying them at present. This applies to the Nasdaq 100 Index and, to a lesser extent, to the S&P 500 and the MSCI World Index. The MSCI AC World IMI Index, which also includes small companies and developing countries, is back at a risk premium of just under 6% and is therefore well suited for new investments.

Equities in Europe, Asia, and developing countries have risk premiums (i.e. target returns) of between 7% and 8% p.a., which is why we are comfortable on the buy side here, even if valuations are no longer as favourable as they were at the beginning of 2025.

Sector Watch: REITs, Healthcare, and Mining

The assessment of the components that were our laggards in 2025, i.e. real estate stocks (REITs), quality factor index ETFs and quality managers, the healthcare sector, and listed private equity companies, is attractive to very attractive overall. It therefore invites us to take a closer look at these investments, which are promising in the long term but disappointing in the short term. They may be low-risk bets for 2026. As for the current enthusiasm for precious metals and copper, we have decided to include ETFs that invest in the relevant mining companies in our advisory universe.

We are not actually fans of non-income-generating “emotional investments” such as gold and Bitcoin, but we cannot deny that there is a changed global situation, especially in the case of gold, which continues to see demand from global central banks.

Since we do not know what will happen to the prices of gold, silver, and copper in 2026, but we do know that mining companies are currently generating a great deal of liquidity that can be used for dividends and share buybacks, we are comfortable with this investment. In addition, the risk premiums here are also around 6–7% p.a., which seems attractive.

Investment Strategy: Mining ETFs and Commodities

We would therefore prefer an investment in mining ETFs to a direct investment in gold or silver. The market for these building blocks is currently undergoing a correction phase, which is probably a good time for new investments. But here, too, please do not blindly chase prices. Instead, pay attention to chart signals or build positions gradually by buying in different tranches.

In general, we consider the addition of commodities via broadly diversified indices or funds to be legitimate but would not want to exceed an overall portfolio allocation of 10–15%.

Sustainable Investing: The Nasdaq Clean Smart Grid Index

In this context, I would also like to mention an index that invests, so to speak, in the shovels and picks of the world’s new energy supply. This is the Nasdaq Clean Smart Grid Index, which can be easily purchased as an ETF from First Trust under the ticker GRID. The index has been calculated since 2009 and includes global companies that represent a sustainable and healthier energy supply. Unlike many poorly structured indices from the “clean energy sector,” this is a portfolio of established and sustainably profitable companies, all of which are market leaders. The index is currently valued at a risk premium of around 6% and has clearly outperformed both the MSCI AC World IMI and the MSCI World Index since 2009. I consider it a good investment for investors who are looking for sustainable investments but do not want to sacrifice returns.

Technology Sector Opportunities

Anyone interested in the technology sector, despite all the valuation issues, should look at Paul Wick, the manager of the CT Global Technology Fund. He has proven that he is capable of successfully investing in technology stocks outside of the Magnificent 7.

Currency Outlook: Stabilising Dollar

As far as currencies are concerned, we also do not know what the new year will bring. However, if we look at the DXY index, which primarily reflects the relationship between the USD and the EUR, the dollar appears to be stabilising somewhat after last week’s sell-off.

Consistency in Investment Styles

As for our three preferred investment styles, we can only emphasise that all three strategies work in the long term, even if their performance can diverge materially in the short term. Investors should therefore stick to their chosen investment styles and not change them randomly.

Please also look at our standard investment portfolio ideas on pages 31 to 33, which follow the principles of investment legends like Jack Bogle, Eugene Fama/Kenneth French and Warren Buffet/Charly Munger. Whilst all of them represent different investment philosophies, they’re all very effective and successful in the long term.

Contact and Community

If you are worried whether your portfolio is well equipped for the significant changes in today’s world, just get in touch with us. We’ll be more than happy to check for you.

Otherwise, I would be delighted if you could tell your friends and family about Das Family Office so that they can also become part of our community.

With best wishes for a wonderful lunar new year!

Appendix I: Expected returns based on current inflation and historic valuations

Real Estate Analogy: Rental Yield

Imagine you are an investor considering buying an apartment to rent out. You want to determine which property offers the best rental yield relative to its purchase price. The rental yield functions similarly to the earnings yield in stocks. It indicates how much rental income you receive annually compared to the purchase price.

Example: Calculating Rental Yield

Property A costs $200,000, and the expected annual rent is $10,000. Rental yield: 10,000 / 200,000 = 5%

Property B costs $400,000, but the expected annual rent is only $12,000. Rental yield: 12,000 / 400,000 = 3%

A high bar in a diagram would indicate that a property offers a high rental yield relative to its purchase price, making it relatively affordable and attractive.

A low bar would indicate that while the property is expensive, it generates only a low rental yield, making it less attractive.

Summary:

High bars = Favorable valuation & good investment opportunity

Low bars = Expensive valuation & low return

While real estate investors assess rental yield in relation to the purchase price, stock investors analyze expected earnings yield relative to the current stock price. However, the objectives for expected returns differ between asset classes.

Bonds: Capital Preservation Through Inflation-Beating Yields

For bonds, it is crucial that their yield exceeds the current inflation rate. If a bond’s interest rate falls below inflation, the investor experiences a real loss in purchasing power.

For example, if a bond provides a 3% annual yield in an environment with 4% inflation, the investor incurs a real loss of 1%. In this case, the investment would be unattractive, as the invested capital loses value over time. In our graph, we illustrate the expected inflation over the next 10 years. This allows investors to quickly assess whether a bond’s current valuation is sufficient to outperform inflation.

Stocks: Evaluating Earnings Yield

Compared to bonds, stocks carry higher risks but also promise higher long-term returns. The key rule is that a stock’s expected earnings yield should be at least 6%, as anything below this threshold suggests an overvalued investment.

This 6% benchmark is based on historical data, which shows that stock markets have generated long-term average returns between 6% and 8% per year. If a stock’s expected return falls below this level, it could indicate that the price is too high relative to its potential earnings—similar to an overpriced property with a low rental yield.

Yours,